All Categories

Featured

Table of Contents

The are whole life insurance policy and universal life insurance policy. The cash value is not added to the fatality advantage.

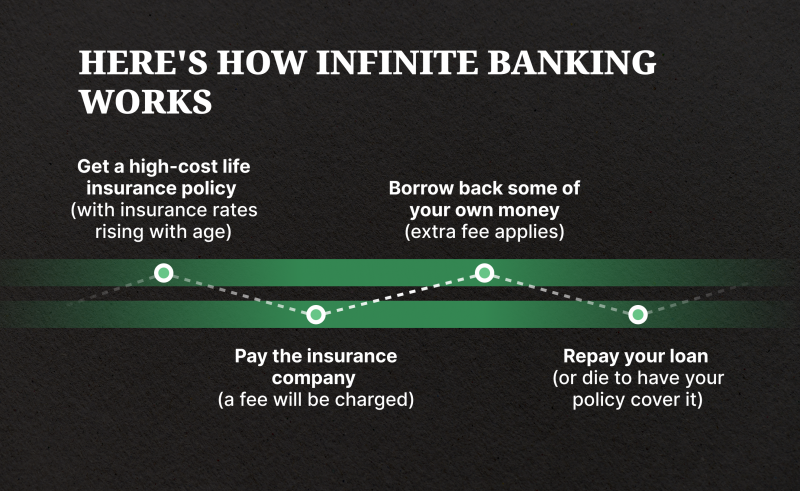

The plan financing rate of interest price is 6%. Going this course, the interest he pays goes back into his policy's money value rather of a monetary establishment.

How To Become My Own Bank

Nash was a money expert and fan of the Austrian school of economics, which supports that the value of items aren't clearly the outcome of conventional economic frameworks like supply and need. Rather, individuals value cash and goods differently based on their financial standing and requirements.

One of the mistakes of typical financial, according to Nash, was high-interest prices on financings. Long as banks established the rate of interest prices and financing terms, individuals really did not have control over their own wealth.

Infinite Banking requires you to own your financial future. For goal-oriented people, it can be the most effective monetary device ever before. Below are the advantages of Infinite Financial: Perhaps the solitary most beneficial element of Infinite Banking is that it improves your cash flow. You don't need to experience the hoops of a traditional bank to get a finance; simply request a policy finance from your life insurance business and funds will be offered to you.

Dividend-paying entire life insurance coverage is really low risk and uses you, the insurance policy holder, a great bargain of control. The control that Infinite Financial uses can best be organized right into 2 categories: tax benefits and asset defenses.

How To Start Your Own Personal Bank

When you utilize entire life insurance policy for Infinite Banking, you get in into an exclusive agreement in between you and your insurance policy company. These defenses may differ from state to state, they can consist of protection from asset searches and seizures, defense from reasonings and protection from financial institutions.

Whole life insurance policy policies are non-correlated possessions. This is why they function so well as the economic foundation of Infinite Banking. Regardless of what occurs in the market (stock, real estate, or otherwise), your insurance plan retains its well worth. A lot of individuals are missing this essential volatility buffer that helps secure and grow wealth, instead dividing their money into 2 containers: bank accounts and investments.

Market-based investments grow wealth much faster yet are subjected to market fluctuations, making them naturally risky. What happens if there were a third bucket that provided safety but also moderate, guaranteed returns? Entire life insurance policy is that 3rd bucket. Not only is the price of return on your entire life insurance policy plan guaranteed, your survivor benefit and premiums are additionally guaranteed.

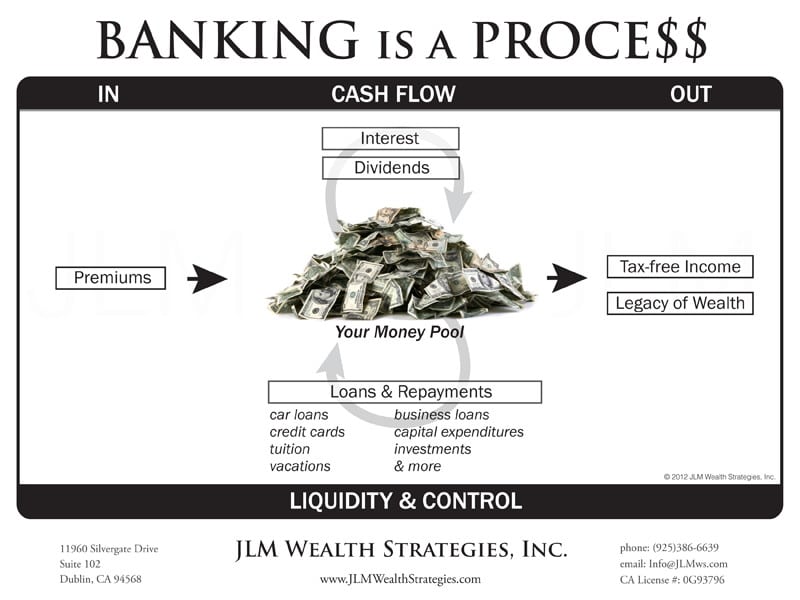

Here are its major benefits: Liquidity and availability: Plan fundings give immediate access to funds without the constraints of standard financial institution lendings. Tax effectiveness: The money worth grows tax-deferred, and plan car loans are tax-free, making it a tax-efficient tool for constructing wealth.

Cibc Visa Infinite Online Banking

Property defense: In many states, the cash money value of life insurance coverage is shielded from creditors, including an added layer of financial safety. While Infinite Financial has its advantages, it isn't a one-size-fits-all option, and it features considerable disadvantages. Here's why it may not be the most effective strategy: Infinite Banking commonly calls for detailed plan structuring, which can perplex policyholders.

Visualize never ever having to fret regarding financial institution financings or high interest prices once more. That's the power of infinite banking life insurance coverage.

There's no set financing term, and you have the liberty to select the payment routine, which can be as leisurely as settling the lending at the time of death. This adaptability includes the servicing of the fundings, where you can go with interest-only payments, maintaining the finance equilibrium flat and convenient.

Holding cash in an IUL taken care of account being credited interest can usually be far better than holding the cash money on down payment at a bank.: You've constantly imagined opening your very own bakeshop. You can obtain from your IUL plan to cover the first expenses of renting out a room, acquiring devices, and working with personnel.

Infinite Financial Resources

Personal lendings can be gotten from conventional banks and credit scores unions. Obtaining money on a credit report card is normally really expensive with yearly percentage prices of interest (APR) commonly getting to 20% to 30% or more a year.

The tax obligation treatment of policy finances can vary dramatically relying on your nation of residence and the details regards to your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, policy lendings are usually tax-free, offering a substantial benefit. In other territories, there may be tax implications to think about, such as possible tax obligations on the loan.

Term life insurance only provides a fatality advantage, without any cash money value accumulation. This suggests there's no money worth to obtain versus.

Nonetheless, for car loan officers, the substantial regulations enforced by the CFPB can be viewed as difficult and limiting. First, lending officers usually say that the CFPB's policies produce unneeded red tape, resulting in more documentation and slower car loan handling. Rules like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) needs, while focused on protecting customers, can lead to delays in shutting bargains and raised operational expenses.

{kind=link}

Latest Posts

Infinity Life Insurance

Infinite Banking Spreadsheets

Infinite Banking Canada